Every investment involves uncertainty: markets rise and fall, and savvy investors know to match their portfolios with their personal risk comfort. Risk tolerance is an investor’s emotional willingness to endure volatility and potential loss in pursuit of returns.

Knowing your risk tolerance and how it differs from risk capacity financial ability to bear losses and risk preference natural inclination toward risk is crucial for building a portfolio you can stick with even in a downturn.

In this guide, we define these terms, give practical examples, and offer a step by step self assessment. We also outline typical asset allocation ranges for conservative, balanced, growth, and aggressive investors and flag common behavioral biases e.g. loss aversion, overconfidence that can skew your risk attitude. By the end, you’ll have concrete tools including a quick quiz to align your investments with your true risk profile and long term goals.

What Is Risk Tolerance?

Risk tolerance is basically how much uncertainty or potential loss you’re okay with if it means you might earn higher returns. In simpler words, it’s your comfort level with the ups and downs of the market. Some people don’t mind big swings at all, they might even enjoy the thrill, while others feel stressed the moment prices start dropping and just want things to stay stable.

You’ll often see formal definitions, like from SEC Investor.gov, saying it’s an investor’s ability and willingness to lose some or all of an investment in exchange for higher potential returns. That’s accurate, but in real life it’s not just about money. It’s also about how you react emotionally. Personality, past experiences, even how you handle stress all play a role. For example, younger investors usually take more risks because they have time to recover, but someone close to retirement might prefer to play it safe.

Let’s take a simple example. Imagine Alice and Bob both invest $100,000. Alice is comfortable with risk, so she puts most of her money into growth stocks and keeps a smaller portion in safer assets. She knows her portfolio might go up and down a lot, and she’s fine with that. Bob, on the other hand, prefers stability. He keeps more money in bonds or cash and less in stocks, even if it means slower growth.

Now, if the market drops by 10%, Alice might just shrug it off and wait it out. Bob, though, could start worrying and think about selling. Same amount of money, similar goals, but completely different reactions. That’s what risk tolerance really looks like in practice.

Risk Capacity and Risk Preference

The difference between risk tolerance, risk capacity, and risk preference must be clear. Risk capacity refers to your financial ability to withstand loss. It is a calculable value and is based on your age, income, total assets, and time until you plan on using these funds. For example, if you are a young person making a lot of money, have little or no debt, and many years ahead of you until you need to draw on your retirement savings, then you could endure a significant amount of loss; therefore, your risk capacity would be high (based upon the example of investing $100,000 and possibly losing $10,000). If, however, you are 55 years old and are about to retire, have a large mortgage, and little to no emergency cash, then your risk capacity would be low. Financial advisors “calculate” risk capacity based upon your savings, debts, and future goals.

Your risk preference (or risk attitude) is how you feel about taking on risk. For some people, they enjoy thrill-seeking and take risks in their personal life, and subsequently will seek high-risk investments; whilst for others, they are risk-averse and take very few risks in their lives and will invest very conservatively. This is the concept of personality and risk tolerance; there is not a direct correlation between risk tolerance and risk preference. A lot of times an advisor will tell you that you have to consider how you feel emotionally about taking on risk and then look at your actual financial capacity to take on risks.

Why both matter: Every investor should have a portfolio that correlates with their risk tolerance and their capacity risk. If you have a high-risk tolerance, but your capacity is low, this could be problematic (i.e., a person who has money, but they are not mentally prepared to risk it could become scared and sell their investment). A financial advisor must work with you to help you determine what you want from your investments vs. what you can afford to put at risk.

Why Risk Tolerance Matters

Your risk tolerance directly affects your portfolio and your ability to reach your long-term investment goals. Your risk tolerance determines how you will allocate your assets (stocks vs. bonds), which investment vehicles you will choose and how you will respond to fluctuations in the stock market from day to day.

For example, an aggressive investor with a high risk tolerance may allocate 80% to 100% of their portfolio to equities for growth. A conservative investor with a low risk tolerance may restrict their equity allocation to approximately 20% to 40%, instead favouring fixed-income and/or cash investments.

Matching your investment strategy to your risk tolerance level can help you avoid making emotionally-driven, panic-based selling decisions during times of volatility. Such panic-based selling can result in costly mistakes. As stated by FINRA, knowing your tolerance for risk allows you to stay committed to a long-term investment strategy, rather than chasing returns, or locking in losses due to fear.

Your investor objectives are also connected to your tolerance for risk. For example, long-term investment objectives (e.g. retirement in 20-30 years) can generally accept a greater level of risk than short-term investment objectives (e.g. paying for college, a down payment for a home) as you have time to recover your losses if you experience a downturn in the stock market. Accordingly, a financial planning solution such as a “bucket” approach — allocating one portion of your portfolio for aggressive, long-term growth and one portion of your portfolio for stable, short-term needs — can help you appropriately align your tolerance for risk with your investment objective.

Assessing Your Risk Tolerance: A Simple Self-Check

Before you invest seriously, it’s worth asking yourself one honest question: how much risk can I actually handle? Not what sounds good, not what others are doing—but what truly fits your mindset and situation.

A good way to figure this out is by thinking through a few realistic scenarios. No need to overcomplicate it—just answer honestly:

- What’s your goal?

Are you trying to grow money over many years, or do you need it soon for something important? - If your investment drops by 10%, what would you do?

Would you buy more, stay calm, or feel the urge to sell? - How important is this money to you?

Is it your main savings, or extra money you can afford to risk? - How would a 20% loss make you feel?

Excited to invest more at a lower price, slightly worried, or very stressed? - What’s your past experience with investing?

Have you stayed calm during market ups and downs, or felt panic?

What Your Answers Mean

Your reactions tell you more than any formula ever could:

- Low risk tolerance

You value safety. Big losses would make you uncomfortable, and you might sell quickly during a crash. - Moderate risk tolerance

You can handle some ups and downs. You may feel nervous at times, but you try to stay invested. - High risk tolerance

You’re comfortable with volatility. You see market drops as opportunities and focus on long-term growth.

Why This Matters

Understanding your risk tolerance isn’t just a “nice to know”—it shapes everything:

- How you invest

- How you react during market crashes

- Whether you stick to your plan or panic

Take a few minutes to reflect or even write down your answers. That clarity can save you from emotional decisions later and help you build a strategy that actually works for you, not someone else.

Investor Profiles & Asset Allocation

Risk tolerance often maps to classic investor profiles. Below are typical asset allocation ranges for each profile, with rationale:

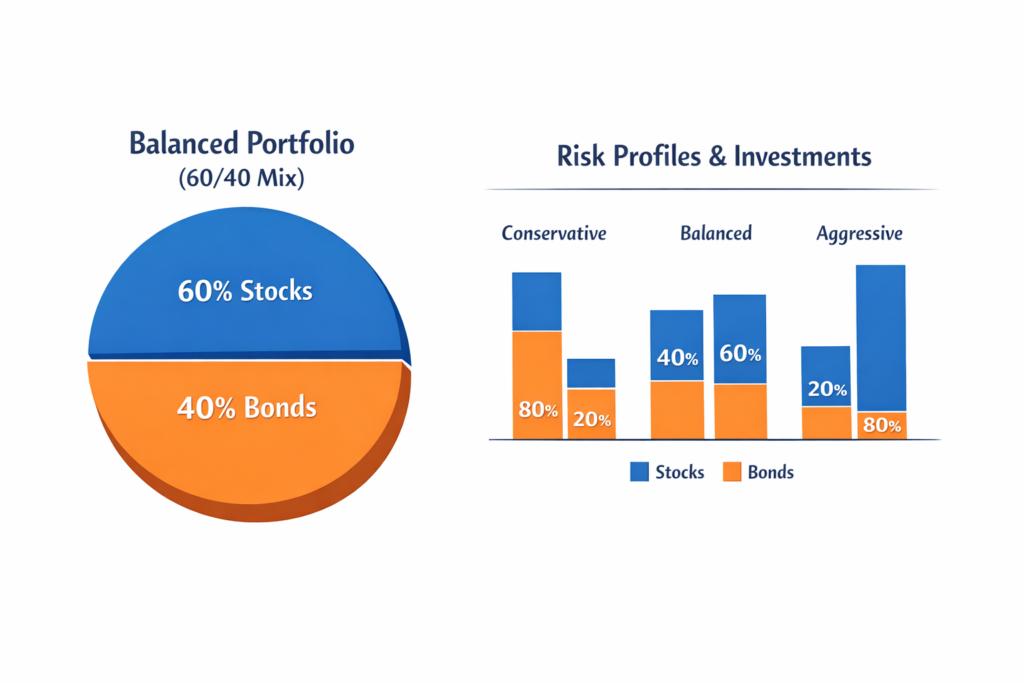

Conservative (Risk Averse): ~20-40% equities and ~60-80% fixed income/cash. Preservation of wealthy is the primary goal when constructing a conservative portfolio. For instance, if a retiree or person approaching retirement chooses 30% in equities (for example, high dividend stocks) and 70% in fixed income/US Treasury securities, they will have a more secure portfolio and are protecting their principal dollar value. It is not uncommon for a “very conservative” portfolio to maintain a small equity exposure to help buy up against inflation.

Moderate/Balanced (Medium Risk): The average balanced investor has ~50-60% equities and ~40-50% fixed income. This “50/50” or “60/40” split is used to create a moderate amount of risk for substantial growth potential, with risk control. Moderate investors tend to overweight equities when the market is rising and bond when the market is declining. According to Investopedia, a balanced stock bond portfolio is generally in the range of approximately 50% stocks and approximately 50% bonds (or 60%/40%, respectively). This strategy should appeal to individuals in their middle career stage trying to build a retirement plan that is 10+ years away.

Growth Investment Strategy (Moderate to Aggressive): Invest between 70-80% in equities (stocks) and, depending on risk tolerance, 20-30% in fixed income (bonds). Investors who have a long investment timeframe, such as young people saving for retirement, typically use 80% in equities (both domestic and international), and 20% in fixed income.

Moderately aggressive portfolios generally qualify for a ratio between 50-50 to 80-20 due to their emphasis on growth; aggressive portfolios can generally use equity ratios greater than 80%.

Aggressive Investment Strategy (High Risk Tolerance): Invest between 85-100% in equities (stocks) as the primary investment; usually not much more than 15% in fixed income (bonds), and normally less than 3% in alternative investments. Examples of aggressive investors include young professionals with very high net worth. Such an investor may be a technology entrepreneur, have recently graduated with a degree, and/or have very limited other stable assets.

All portfolios will fall somewhere along these ranges; the choice for an individual investor will depend on other asset classes, like net worth and diversification. An investor who has a high income and few other stable assets (such as home equity and a pension) is generally able to tolerate a large stock tilt (a higher capacity for risk).

Many advisor model portfolios display similar equity/bond splits; conservative models typically have bonds making up a higher percentage of the total portfolio, while aggressive models show a greater percentage of the total portfolio in equities.

Behavioral Biases and Risk Tolerance

A clearly defined risk profile can still be glossed over due to some inherent bias in people’s thinking. Behavioral bias, which refers to how our way of thinking distorts our ability to make rational choices when it comes to risk. The most common forms of bias that influence an investor’s tolerance for risk are:

Loss aversion: An investor feels the emotional effects of losing far worse than those experienced by them as a result of gaining an equivalent amount of wealth. Loss averse investors frequently misjudge their risk tolerance by overreacting to potential losses. For example, an investor may say he/she can deal with risk; however, when the market drops 20%, they lose their composure and sell. One way to manage this is to frame the decisions positively (considering what the investor has to give up if he or she decided not take the risk), and from time to time, as opposed to at an emotional point in time, review your goals.

Recency bias: An investor tends to put greater emphasis on recent events. As a result of an upward price trend, the investor may experience an inflated sense of confidence and invest in a large number of high-risk investments; conversely, an investor may adopt an overly conservative position as a result of a downward price trend. Because of this, an investor should follow their investment plan based upon a specific set of financial goals; and always keep in mind the average annual returns over the past 30 years when evaluating an investment’s future investment performance. For example, even in the most recent bull markets, no investment is guaranteed a “safe” return.

Overconfidence & Herding: Thinking you can “beat the market” or following the crowd. Overconfident investors overestimate their tolerance and often take excessive risk

. Herding (following peers or media) can push someone into risky investments unsuited to their profile. To counteract, focus on education: understand each investment’s risk (e.g., emerging markets or crypto are high-risk) and maintain a diversified portfolio.

Anchoring: Relying on a specific reference point (e.g. original purchase price) can skew risk tolerance. If you anchor to past prices, you might cling to losing stocks hoping they’ll “come back”, ignoring your true tolerance. Mitigate by setting entry and exit rules beforehand or using “stop-loss” orders.

Familiarity Bias: Preferring known assets (e.g. your company’s stock or local market) leads to under-diversification. Comfort with “what you know” limits your portfolio’s risk profile. Combat this by researching unfamiliar assets and gradually adding international or sector funds to diversify and align with your stated risk level

Generally, it is a good idea to recognize your emotions. “A useful technique is for you and your advisors to openly discuss your biases so that you will be able to make better decisions.” In order to help prevent panic selling, make certain that you have a pre-determined schedule to regularly rebalance your investments. Create a portfolio that can be divided according to specific goals (e.g., retirement and/or emergency fund) and the time frames in which you want to achieve those goals. Doing so will allow you to maintain your goal-related portfolios separately, which will lower the chances of your entire plan being disrupted by an emotional (panic) reaction to market volatility.

Conclusion and Next Steps

Understanding your risk tolerance – and keeping it aligned with reality – is vital for long-term investing success. In summary:

- Define your tolerance (emotional comfort) and your capacity (financial ability) Both affect how much risk you should take.

- Assess it honestly with a quiz or checklist (like the one above), considering goals, horizon, and past reactions

- Choose an asset mix that reflects your profile. Conservative portfolios (e.g. 20/80 stocks/bonds) suit low tolerance, while aggressive portfolios (80%+ stocks) suit high tolerance

Rebalance periodically to maintain this mix. - Watch for biases Know common pitfalls like loss aversion and recency bias, and use rules or advisor guidance to stay on track.

- Re-evaluate regularly Life changes (new job, marriage, market swings) can shift your tolerance and capacity. Update your strategy and allocations accordinglyBy following this guide – and consulting with financial professionals when needed – you can align your investments with both your personal comfort and your financial goals

Investment Risk Tolerance – FAQs

What is risk tolerance in investing?

Risk tolerance is the level of uncertainty or market fluctuation an investor is comfortable handling.

It helps determine how much risk you can take when making investment decisions.

Why is risk tolerance important?

It ensures your investment strategy matches your financial goals and emotional comfort.

Without understanding it, you may panic during market downturns or take unnecessary risks.

What are the types of risk tolerance?

There are three main types: conservative, moderate, and aggressive. Conservative investors prefer stability,

while aggressive investors are willing to take higher risks for potentially higher returns.

How can I measure my risk tolerance?

You can evaluate it based on your income, financial goals, time horizon, and how you react to losses.

Many investors also use online assessment tools for guidance.

Does risk tolerance change over time?

Yes, it can change due to life events, financial situations, or experience in the market.

Regular reviews are recommended.

Is higher risk always better?

No. Higher risk may bring higher returns, but it also increases the chance of loss.

The best approach is to balance risk with your personal comfort and long-term goals.

Leave a Reply